Here’s What Happened to Real Estate Markets The Last Time Interest Rates Dropped in the US

Since the Federal Reserve began raising interest rates in 2022, prospective homebuyers and economists alike have been trying to predict when rate cuts may be coming. Currently, the federal funds rate is at 5.50% and average 30-year mortgage rates are around 6.82%. As borrowing costs increased, national home sales slowed. But if rates do drop this year, how will it impact real estate markets?

To better understand what could be in store for 2024, Zoocasa has taken a historical look at what happened the last time the Federal Reserve dropped interest rates in 2019 and the impact it had on home prices and sales.

2019: The First Rate Cut in Over 10 Years

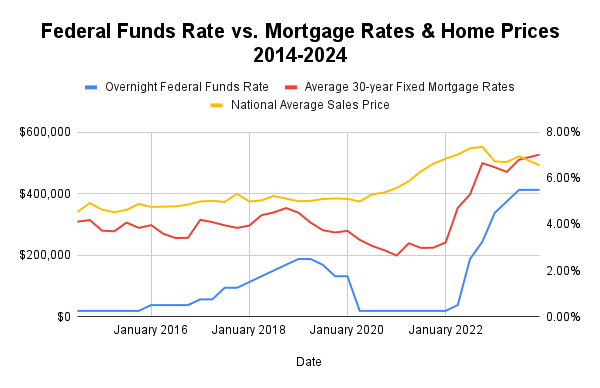

The US real estate market was relatively predictable from 2009 until May 2017, with the federal funds rate below 1.00%. Even as interest rates gradually rose in 2017 and 2018, the national average sales price and national home sales remained stable, without any major increase or decrease. It wasn’t until after interest rates dropped in 2019 that both home sales and prices started to experience turbulence.

In July 2019, long before the pandemic started, the Federal Reserve lowered the federal funds rate from 2.5% in June to 2.25% in July, marking the first rate cut since September 2008. This was followed by two additional rate cuts in September and October of the same year, bringing down the federal funds rate to 1.75% in December 2019.

However, the initial drops in the federal funds rate did not bring immediate spikes in home sales and home prices. Following the three interest rate cuts, national home sales increased year-over-year by 8.8% to 5,450,000 in December 2019, and the national average home price was just 0.2% higher than the year before at $375,500. This indicates that if interest rates do drop in 2024, there may be a few weeks or months’ delay in the response in the real estate market. Homebuyers who act quickly may even be able to snag a deal when both home prices and mortgage rates are lower.

The Aftermath of Extremely Low Interest Rates

In April 2020, the Federal Reserve lowered the federal funds rate from 1.25% in March to 0.25%. In the following months, this drastically impacted buyer demand, quickly pushing up sales and prices to new highs.

With average 30-year mortgage rates between 2.65% and 3.22% in 2021 and 2022, homebuyers jumped at the opportunity to buy a property for lower borrowing costs. In April 2020, national home sales were at a low of 4,460,000, but by October 2020 they had shot up to 6,560,000 – a jump of 47.1% in just six months. In January 2021, national home sales peaked with 6,600,000 sales.

As more and more buyers flooded into the market, average home prices continuously climbed. In Q2 2020, the national average home price was at $374,500 and six months later it had risen by 7.9% to $403,900. After persistently climbing for another two years, the national average home price peaked in Q4 2022 at $552,600. That comes out to a 47.6% increase in the national average home price from Q2 2020 to Q4 2022.

So what does this mean for homebuyers in 2024? Once momentum starts building for lower borrowing costs, the real estate market will get increasingly more active. Competition for in-demand properties will especially skyrocket and this increased urgency from buyers will also maintain upward pressure on home prices. Getting ahead of the surge in buyer activity could be a strategic move for those able to secure financing ahead of time.

So When Will Interest Rates Drop in 2024?

The latest inflation figures show that US inflation increased from 3.2% in February to 3.5% in March. This could mean that rate cuts may be further out than previously anticipated. The Federal Reserve has indicated that they are prepared to hold the rate at 5.5% until inflation is more confidently trending downward.

Though mortgage rates are not yet as low as many homebuyers would want, they have come down quite a bit. At the end of 2023, the average 30-year fixed rate was above 7.6% and current averages are hovering under 7%. Home prices have also softened significantly from 2022, with the average sales price dropping from $521,900 in Q3 2023 to $492,300 in Q4 2023. So though borrowing costs remain high, conditions for homebuying are not necessarily unfavorable now.

Zoocasa (April 11,2024)