10-Year Review: How an Interest Rate Drop Could Affect Real Estate Markets

After increasing the overnight lending rate ten times between March 2022 and July 2023, many are expecting the Bank of Canada to start implementing rate cuts later this year. The overnight lending rate is currently at 5%, the highest in more than a decade, and has caused many fixed mortgage rates to similarly reach record highs. This slowed real estate activity in the second half of 2023, but with many optimistic that interest rate cuts are on the horizon, buyer interest seems to be picking up again.

So if interest rates do drop later this year, how will it impact the real estate market? To better understand what could be in store for 2024, Zoocasa has taken a historical look at what happened when the Bank of Canada lowered its overnight lending rate in 2015 to today using data from the Canadian Real Estate Association.

The Ripple Effects of Rate Cuts on Sales and Home Prices

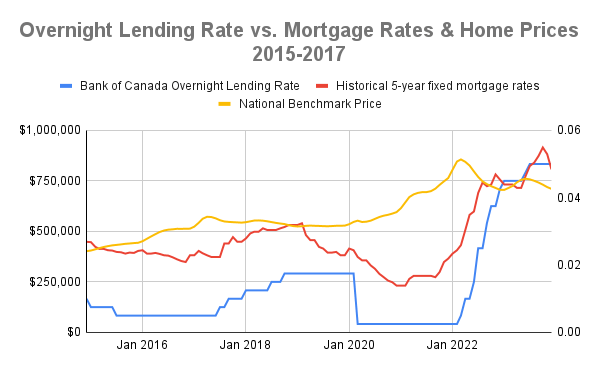

After staying at 1.0% for more than four years, the Bank of Canada dropped the overnight lending rate to 0.75% in January 2015 in response to plunging oil prices. The rate remained at 0.75% until July 2015 when the rate dropped again to 0.5%. At the time, economic growth was slowing and consumer-energy products were experiencing year-over-year price declines. The Bank of Canada held the overnight lending rate at 0.5% for the following two years until eventually raising it to 0.75% in August 2017. So what impact did this rate cut have on the housing market?

The decrease in the overnight lending rate did not cause fixed-rate mortgages to immediately drop, but rather the effects took several months to reflect in mortgage rates. One month after the initial drop to 0.75%, the historical 5-year fixed mortgage rate decreased from 2.68% in January 2015 to 2.54% in February 2015, but three months after the initial drop the 5-year fixed mortgage rate was down to 2.48%. The 5-year fixed mortgage rate didn’t reach its lowest point until 22 months after the first rate cut, when it fell to 2.09%. Considering this, if the Bank of Canada does lower the overnight lending rate this year, then it might take anywhere from a few months to over a year for fixed mortgage rates to experience a significant decrease.

However, home prices and sales experienced the opposite effect. As the overnight lending rate came down, the national benchmark price and sales started inching upwards. From the first rate cut in January 2015 to just before the second rate cut in July 2015, the national benchmark price increased by 6.3%. But a year after the second rate cut in July 2015, the national benchmark price increased by 17.4%. In total, from the first rate cut in January 2015 to just before rates increased again in July 2017, the national benchmark price increased by 39.3%. This suggests buyers who are waiting for rate cuts may miss opportunities for more affordable pricing, as rising demand caused by a rate drop will likely drive prices upwards.

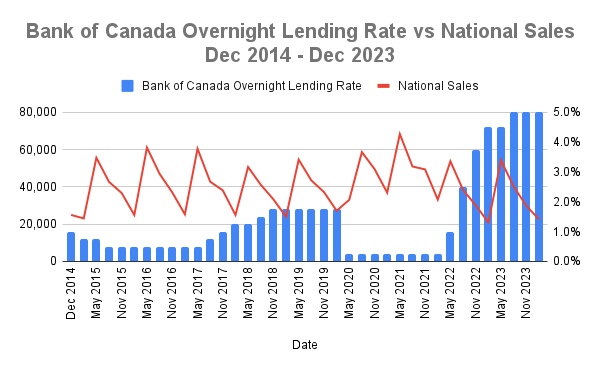

Increasing prices didn’t stop homebuyers from entering the market, and in fact, national sales steadily increased. The real estate market was impacted by the normal ebb and flow of the seasonal cycle, so there were drops in sales in the winter months, however in the spring of each year of the rate cuts national sales soared. May 2015 was the first peak in national sales, just four months after the first rate cut, with national sales increasing by 141.1% from January 2015 to May 2015. National sales increased even more in May 2016, when national sales rose from 55,619 in 2015 to 61,097 – a jump of 9.9%.

2020 – 2023: The Pandemic Effect on Mortgage Rates and Market Activity

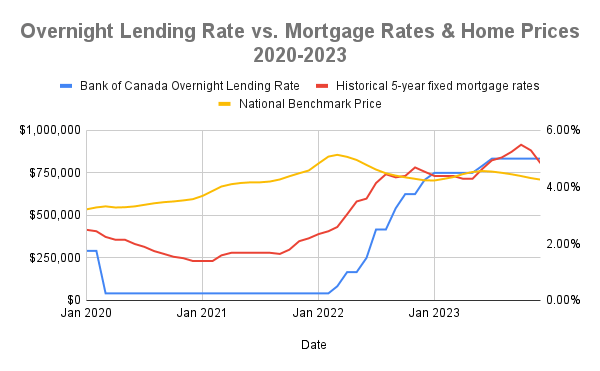

The COVID-19 pandemic brought on a lot of unprecedented changes, and that rang true for the economy too. For all of 2019, the Bank of Canada held the overnight lending rate at 1.75%, but in March 2020, the Bank decided to lower the overnight lending rate to 0.25% – the lowest in ten years. Similar to when the Bank lowered rates in 2015, in 2020, 5-year fixed mortgage rates came down and the national benchmark price climbed up.

Just like in 2015, there was a slight lag in the drop of 5-year fixed mortgage rates. Two months after the first drop, the 5-year fixed mortgage rate fell from 2.24% to 2.14%. However, nearly one year after the first rate drop, the 5-year fixed mortgage rate decreased to 1.39%. This further indicates that when the Bank of Canada does decide to lower the overnight lending rate, it will take some time for fixed mortgage rates to follow.

Despite the economic uncertainty of the time, the national benchmark price consistently increased from 2020 to 2022 and outpaced the rate of growth experienced from 2015 to 2017. From the first rate cut in March 2020 to just before rates were raised again in March 2022, the national benchmark price increased by 52.9%. As time went on and buyers gained more confidence in the market, the increased buyer activity sustained continued price growth. Prospective buyers looking to enter the market this year might consider doing so before any rate cuts by the Bank of Canada are announced, to avoid the likely surge in home prices and competitive bidding that could follow.

Zoocasa (Mackenzie Scibetta, February 12,2024)